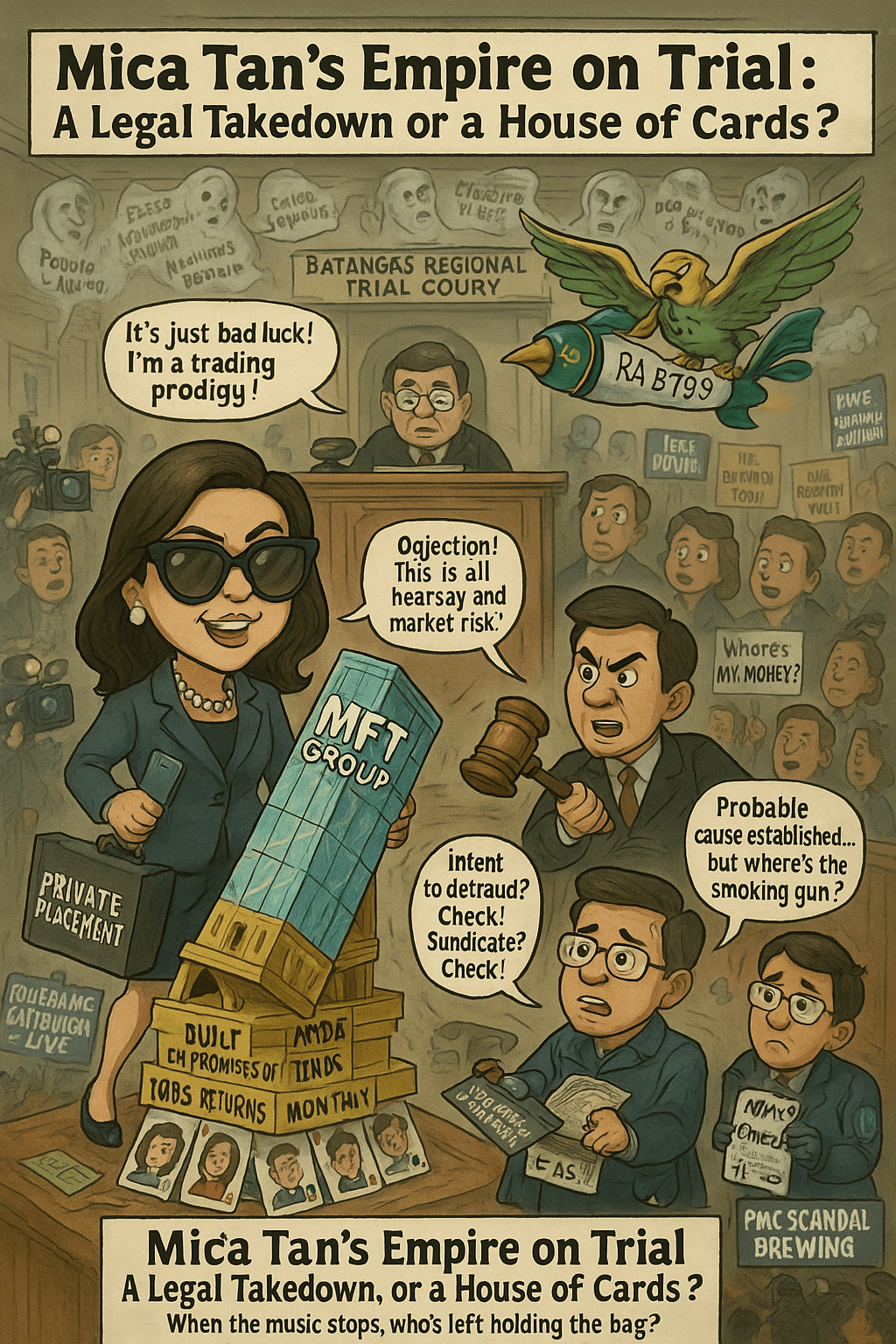

By Louis ‘Barok‘ C. Biraogo — May 14, 2025

THE Batangas Regional Trial Court’s (RTC) arrest warrant against Maria Francesca “Mica” Tan-Cancio and seven others for syndicated estafa, paired with the Securities and Exchange Commission’s (SEC) scorching complaint for unlicensed investment schemes, has ignited a firestorm in the Philippines’ financial world. Toss in the SEC’s bombshell accusation against Isla Lipana & Co., a PwC affiliate, for allegedly rubber-stamping MFT Group’s shady financials, and you’ve got a legal spectacle brimming with fraud, audacity, and regulatory fury. This Kweba ng Katarungan analysis, dripping with skepticism, rips apart the case’s legal foundation, defense ploys, ethical sinkholes, and seismic implications. Buckle up: the prosecution’s got a strong hand, but the defense is ready to roll the dice.

1. Charges Unraveled: Ironclad Case or Shaky Ground?

The charges against Tan and her crew rest on two legal juggernauts: syndicated estafa under Article 315, Revised Penal Code (RPC) and Presidential Decree No. 1689 (PD 1689), plus violations of the Securities Regulation Code (SRC, RA 8799). Let’s tear into them.

Syndicated Estafa: A Slam-Dunk Fraud Scheme?

Syndicated estafa demands (1) estafa via false pretenses, (2) a syndicate of five or more, and (3) public defrauding through fund misappropriation. The prosecution’s case looks tailor-made:

- Eight-Deep Syndicate: Tan and seven co-accused check the syndicate box, hinting at a coordinated con.

- NDAs Scream Cover-Up: Forcing investors into non-disclosure agreements (NDAs) smells like a ploy to hide dirty deeds.

- Courtroom Backing: People v. Aquino (G.R. No. 234818) saw the Supreme Court nail officers for syndicated estafa over fake investment promises. People v. Mateo (G.R. No. 210612) doubled down, flagging sky-high return pledges as fraud red flags.

Strengths: The eight accused and NDAs build a fortress around the syndicate and deceit claims. Investor losses cement misappropriation.

Weak Spots: Proving intent to defraud is the prosecution’s Achilles’ heel. If Tan’s team can spin losses as market misfires or show some legit investments, the case wobbles. The NDAs’ fine print—standard or sinister?—could also stir confusion.

SEC Violations: Caught Red-Handed or Technicality Trap?

The SEC accuses Tan’s group of hawking investments without a license, breaching Section 8.1, RA 8799, which demands securities registration before public sales. Section 28 slaps violators with fines and jail time.

- Nailed on Facts: MFT’s alleged mass solicitation without SEC approval is a textbook violation. Investment contracts, per Section 3.1, cover schemes promising profits from others’ work—Tan’s trading empire in a nutshell.

- Legal Muscle: SEC v. Oudine Santos (G.R. No. 195542, 2014) upheld the SEC’s power to crush unlicensed solicitations, with exemptions interpreted tightly.

Strengths: If MFT pitched to the masses (think social media blitzes), the SEC’s case is bulletproof. The scheme’s scale screams public offering.

Weak Spots: The defense might claim a “private placement” exemption under Section 10.2, but that’s a long shot unless they prove a tiny, elite investor pool. Vague details on MFT’s marketing tactics could give the defense an opening.

2. Defense Playbook: Desperate Moves or Clever Counters?

Tan’s legal squad, led by Atty. Estrella Elamparo, will likely swing hard. Here’s their probable game plan—and why it might crash and burn.

“No Fraud, Just Bad Luck”

- Plea: “We meant no harm. Market crashes, not fraud, tanked the investments.”

- Takedown: People v. Aquino says promising unrealistic returns while knowing the scheme’s doomed shows intent. NDAs hint at hiding the truth, not honest mistakes. Flaw: Proof of siphoned funds (e.g., lavish personal spending) would torch this defense.

“No Syndicate, Just a Team”

- Plea: “Not all eight were conspiring. Some were just staffers.”

- Takedown: People v. Balasa notes syndicates need coordinated action, not equal guilt. MFT’s shared roles (marketing, fund handling) scream conspiracy. Flaw: With eight players, proving no unified scheme is a pipe dream.

“Private Deal, No SEC Needed”

- Plea: “This was a private placement, exempt from SEC rules.”

- Takedown: SEC v. Oudine Santos limits exemptions to small, controlled offerings. Broad pitches, even to a few dozen, demand registration. Flaw: Tan’s “trading prodigy” hype likely reached the public, sinking this argument.

“Auditors Acted in Good Faith”

- Plea (Isla Lipana): “We trusted MFT’s numbers and followed auditing rules.”

- Takedown: Tayag v. CA (G.R. No. 95229 June 9, 1992) holds auditors liable for missing major misstatements. Clean opinions on bad financials suggest negligence, if not worse. Flaw: GAAS demands skepticism; leaning on MFT’s data without scrutiny won’t fly.

“Warrant’s Bogus”

- Plea: “The arrest warrant lacks judicial probable cause, or the prosecutor’s preliminary investigation failed to establish reasonable certainty of conviction.”

- Takedown: Rule 113, Rules of Court requires judges to find probable cause for arrest warrants, based on the prosecutor’s resolution and evidence. However, under DOJ Circular No. 015 (2024), prosecutors must establish prima facie evidence with reasonable certainty of conviction in preliminary investigations for crimes like syndicated estafa. The RTC’s swift warrant issuance suggests both standards were met, supported by the SEC’s complaint. Flaw: Overturning a warrant requires showing clear procedural errors (e.g., no preliminary investigation or grossly insufficient evidence), unlikely given the case’s high profile and DOJ/SEC scrutiny.

3. Ethical Firestorm & Regulatory Shockwaves: Who’s Burned?

Isla Lipana’s Moral Meltdown

Isla Lipana & Co.’s alleged role is a stain on auditing ethics, violating RA 9298 and the Code of Ethics for Professional Accountants. Greenlighting MFT’s 2020–2021 financials despite “inconsistencies” raises questions of negligence or complicity.

- Legal Peril: Tayag v. CA confirms auditors face liability for missing material errors. If Isla Lipana ignored red flags (e.g., fake revenues), they risk fines, license loss, or lawsuits under RA 9298, Section 29.

- Ethical Stain: The Philippine Standards on Auditing (PSA) demand rigorous scrutiny. Collusion, as the SEC hints, could tank PwC’s local cred.

SEC’s Power Play: Crackdown or Overreach?

The SEC’s aggressive moves—nailing MFT and dragging a Big Four affiliate into the fray—mark a bold new era. Unlike SEC v. Oudine Santos, which targeted small fry, this case takes aim at heavyweights.

- Precedent Fit: The SEC’s investor-protection focus aligns with Oudine Santos, but auditing scrutiny is a fresh twist.

- Ripple Effects: This could scare off scam artists and force auditors to shape up. But vague “public offering” rules might spook legit startups, stifling innovation.

4. Battle Plan: Winning Moves for All Sides

Prosecutors: Go for the Jugular

- Prove the Syndicate: Use NDAs, emails, and bank records to show the eight accused worked as a unit. People v. Aquino says shared roles are enough.

- Expose Lies: Dig into MFT’s financials and investor claims. Gaps between promised and real returns scream fraud.

- Slam Isla Lipana: Subpoena audit papers to reveal missed red flags, building a case for negligence or collusion under RA 9298.

Defendants: Damage Control

- Plea Deal: If fraud evidence is ironclad, cut deals to dodge PD 1689’s life sentence, settling for simple estafa.

- Quash Motion: Move to quash the information by arguing the complaint fails to establish prima facie evidence with reasonable certainty of conviction, such as insufficient admissible evidence of investor harm or syndicate coordination. This is a long shot given the SEC’s allegations and judicial review but may delay proceedings.

- Auditor Pivot: Isla Lipana should tout GAAS compliance and blame MFT’s lies. Expert witnesses on audit limits could soften the blow.

Regulators: Fix the System

- Tighten Rules: Clarify “public offering” and “private placement” in RA 8799 to close scam loopholes.

- Audit Watchdog: Boost PRC oversight to catch sloppy audits before they enable fraud.

- Educate Investors: Use MFT’s fall to warn against too-good-to-be-true schemes.

Showdown Snapshot: Charges vs. Defenses

| Issue | Prosecution’s Arsenal | Defense’s Counter | Precedent/Weakness |

|---|---|---|---|

| Syndicated Estafa | 8 accused + NDAs prove conspiracy; losses show fraud. | “No intent; market losses.” | People v. Aquino: High returns + cover-up = fraud. Fund misuse kills defense. |

| SEC Violation | Unlicensed public pitches; broad marketing clear. | “Private placement, no license needed.” | SEC v. Oudine Santos: Public offers need registration. Public hype dooms defense. |

| Auditor Liability | Clean audits on bad books; SEC smells collusion. | “Trusted MFT’s data, followed GAAS.” | Tayag v. CA: Negligence if red flags missed. Blind trust no excuse. |

Final Verdict: A Financial Reckoning Awaits

Mica Tan’s MFT Group saga is a cautionary tale of greed, deception, and regulatory wrath. The prosecution’s case for syndicated estafa and SEC violations, backed by People v. Aquino and SEC v. Oudine Santos, stands on solid ground, with NDAs and financial lies as smoking guns. Defenses like “no intent” or “private deals” look like hail-Mary passes against a tidal wave of evidence. Isla Lipana’s audit fumble could redefine auditor accountability, while the SEC’s bold stance heralds a crackdown on financial cowboys.

But cracks remain: Can intent be proven beyond doubt? Will Isla Lipana slip through with a good-faith plea? And can regulators seal the gaps that let MFT flourish? Tan’s empire is teetering, but the legal fallout will reshape the game. Watch this space—this drama’s just heating up.

Disclaimer: This is legal jazz, not gospel. It’s all about interpretation, not absolutes. So, listen closely, but don’t take it as the final word.

- “Forthwith” to Farce: How the Senate is Killing Impeachment—And Why Enrile’s Right (Even If You Can’t Trust Him)

- “HINDI AKO NAG-RESIGN!”

- “I’m calling you from my new Globe SIM. Send load!”

- “Mahiya Naman Kayo!” Marcos’ Anti-Corruption Vow Faces a Flood of Doubt

- “Meow, I’m calling you from my new Globe SIM!”

- “No Special Jail for Crooks!” Boying Remulla Slams VIP Perks for Flood Scammers

- “PLUNDER IS OVERRATED”? TRY AGAIN — IT’S A CALCULATED KILL SHOT

- “Several Lifetimes,” Said Fajardo — Translation: “I’m Not Spending Even One More Day on This Circus”

- “Shimenet”: The Term That Broke the Internet and the Budget

- “We Did Not Yield”: Marcos’s Stand and the Soul of Filipino Sovereignty

- “We Gather Light to Scatter”: A Tribute to Edgardo Bautista Espiritu

- $150M for Kaufman to Spin a Sinking Narrative

Leave a comment