Gatekeepers Turned Doormen: Why Remulla Is Right to Threaten Cases Against the AMLC

By Louis ‘Barok‘ C. Biraogo — March 27, 2026

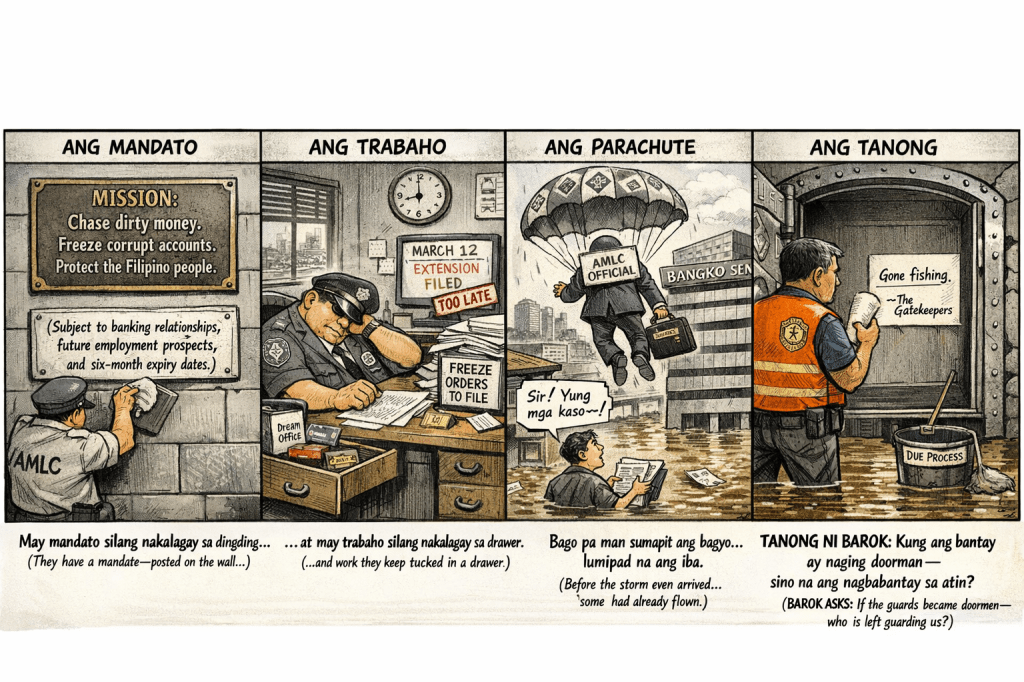

WE, the long-suffering taxpayers who watch our flood-control billions vanish into ghost projects while Metro Manila drowns every rainy season, owe Ombudsman Jesus Crispin “Boying” Remulla a stiff drink and a standing ovation. On March 26, 2026, he did what every self-respecting graft-buster should do: he looked the Anti-Money Laundering Council (AMLC) straight in the eye and said, in plain Filipino, what we’ve all been screaming since the first “pork” scandal: there is a problem with how some of you are performing your duties. Specifically, the Executive Director, the Council itself, and the institutional reflex to coddle the very banking industry it is supposed to drag into the sunlight.

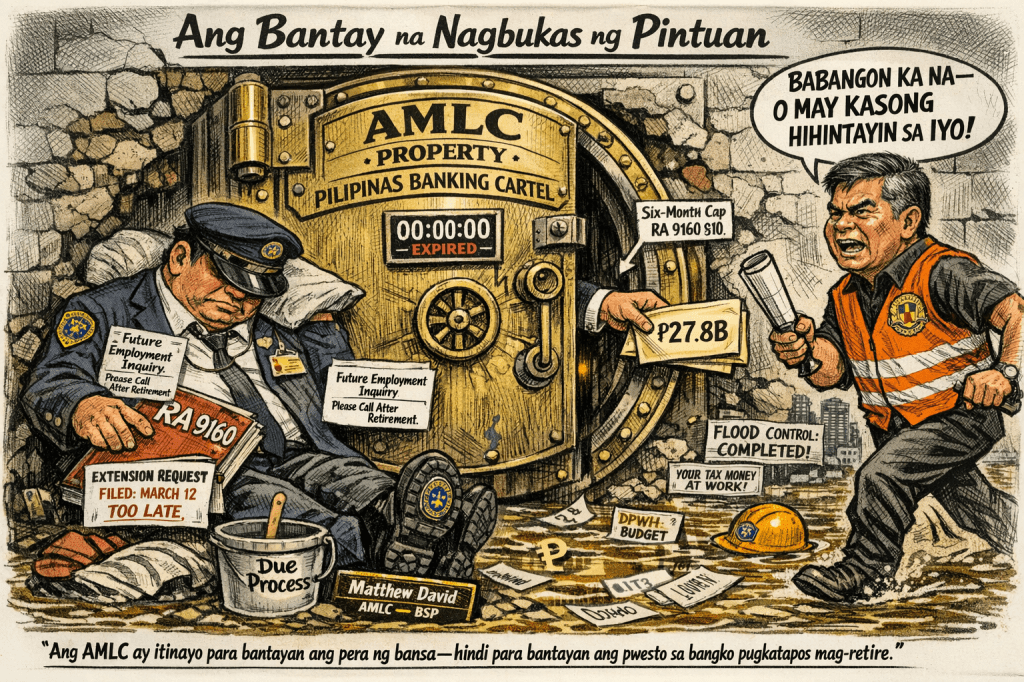

This is not a turf war. This is the public manifestation of a fatal design flaw in our anti-corruption architecture. The AMLC’s statutory duty under Republic Act No. 9160 (Anti-Money Laundering Act of 2001) (as amended by Republic Act No. 11521 (An Act Further Strengthening the Anti-Money Laundering Law)) is to chase dirty money, issue freeze orders, and file civil forfeiture cases. Instead, it has cultivated an institutional culture that treats banks as sacred clients rather than potential co-conspirators in plunder. Remulla’s public broadside is not petulance; it is a calculated, high-stakes gambit to shatter the protective wall and force the AMLC to choose: cozy relationship with the banking cartel or its legal mandate. The man just named names. Matthew David. The revolving door. The quiet transfer back to Bangko Sentral ng Pilipinas (BSP) the day before Remulla spoke. If that isn’t a parachute jump from a plane already on fire, I don’t know what is.

Revolving Door Parachute: RA 6713 Is a Mere Suggestion

Let us be brutally precise. Republic Act No. 6713 (Code of Conduct and Ethical Standards for Public Officials and Employees), Section 7, prohibits exactly this kind of conflict: accepting employment in a private enterprise regulated, supervised, or licensed by the official’s office. The AMLC secretariat is housed at the BSP. Its officials rub shoulders daily with the very banks whose accounts they freeze (or, more often, fail to freeze fast enough). David’s convenient homecoming to the BSP is not “routine personnel movement.” It is the living embodiment of regulatory capture.

Remulla didn’t mince words: “Perhaps some of them still want to have friends in the banking industry so they can move there once they leave the AMLC.” He is right. The post-employment ban under RA 6713 is toothless. We need a mandatory five-year iron wall—no AMLC official who touched a file may waltz into any bank they supervised. Anything less is an engraved invitation to look the other way while ₱27.8 billion in suspicious assets sit in 7,970 bank accounts.

“Caution” or Complicity? AMLC’s Deadly Delays Exposed

The Court of Appeals just handed the AMLC a stinging denial in CA GR-AMLA 00432 (resolution dated March 16, 2026). Extension for a freeze order covering over a hundred accounts tied to the Bulacan ghost projects? Denied. The six-month cap under RA 9160, Section 10 (as amended) is not a suggestion; it is a guillotine. The AMLC knew the clock was ticking. It sought the extension on March 12. Too little, too late. Result? A window opened for the accused to breathe easier, even if Deputy Ombudsman Mico Clavano’s asset preservation orders in the three civil forfeiture cases already filed are keeping some money technically “frozen.”

This is not judicial nitpicking. This is operational malpractice. While corrupt officials and contractors launder flood-control kickbacks at warp speed, the AMLC moves at the pace of a government clerk filling out a form in triplicate. The same RA 9160 that gives the AMLC ex parte freeze power and bank inquiry authority (Section 11) also demands it use those tools aggressively when predicate offenses—Republic Act No. 3019 (Anti-Graft and Corrupt Practices Act) graft, Republic Act No. 7080 (An Act Defining and Penalizing the Crime of Plunder) plunder—are screaming from every DPWH budget line. Instead, we get invocations of “due process” and “bank secrecy” as though these were sacred talismans rather than statutory shields that the AMLC itself is empowered to pierce.

Contrast this with the Ombudsman’s imperative. Republic Act No. 6770 (The Ombudsman Act of 1989) and the 1987 Constitution of the Republic of the Philippines demand relentless investigation. Remulla is not asking the AMLC to break the law; he is demanding it stop treating the law like a polite suggestion.

Freeze-to-Forfeiture Fiasco: AMLC’s Bottleneck Laid Bare

Let us dissect the prosecutorial pipeline with the cold scalpel it deserves. A Court of Appeals freeze order is temporary preventive medicine—maximum six months, ipso facto lifted if no case is filed. Civil forfeiture in the Regional Trial Court is the real hammer: an in rem proceeding under the Rules of Procedure in Cases of Civil Forfeiture where the State only needs probable cause, not proof beyond reasonable doubt.

The AMLC has frozen ₱27.8 billion. It has filed three civil forfeiture petitions. Three. That is not a pipeline; that is a dripping faucet. Why are the bulk of those assets not already the subject of RTC forfeiture cases with provisional asset preservation orders secured before the CA freeze lapsed? The AMLC knows the drill. It knows Republic v. Eugenio Jr. (G.R. No. 174629, 2015) and Subido Pagente Certeza Mendoza & Binay Law Offices v. CA (2013) require procedural safeguards—but those cases also affirm that once probable cause is established, the AMLC must move like the financial SWAT team it claims to be, not a debating society.

The distinction is not academic. Every day the transition from freeze to forfeiture drags, the structural contradiction widens: RA 3019 and RA 7080 scream for blood, while Republic Act No. 1405 (An Act Prohibiting Disclosure of or Inquiry into, Deposits with any Banking Institution and Providing Penalty Therefor) and Republic Act No. 6426 (Foreign Currency Deposit Act of the Philippines) keep the veins of laundered wealth intact behind impenetrable bank secrecy.

Structural Schizophrenia: Graft Demands Blood, Banks Get Fortresses

This is the central thesis no one in the polite corridors of power wants to utter aloud. Our legal architecture suffers from clinical schizophrenia. On one side, the anti-graft and plunder laws demand aggressive financial tracing. On the other, bank secrecy laws—untouched by meaningful reform—create fortresses for the proceeds of crime. The AMLC sits precisely at the fault line, structurally incentivized to hesitate, to “balance” stakeholder interests, to preserve “banking stability” while taxpayers’ money for flood control is siphoned into 15 contractors’ pockets.

The result is predictable: freeze orders lapse, extensions are denied, civil forfeiture crawls, and the next flood washes away both the evidence and the public’s remaining faith.

Prosecute the Protectors: Time for Radical Legal Surgery

Remulla has already drawn the line: “otherwise we will file a case against them.” He is correct. Article 208 of the Revised Penal Code (neglect of duty) and RA 3019, Section 3(e) (causing undue injury through manifest partiality or evident bad faith) are not decorative. If evidence of deliberate foot-dragging or conflict of interest emerges, the Ombudsman must indict AMLC officials with the same ferocity it reserves for DPWH ghosts.

Legislative surgery is non-negotiable:

- Amend RA 9160: remove the six-month freeze cap for plunder and large-scale graft cases certified by the Ombudsman, or make extensions presumptive upon certification.

- Iron wall on the revolving door: mandatory five-year ban under RA 6713 for AMLC officials from any bank or financial institution they supervised.

- Automatic suspension of bank secrecy upon Ombudsman certification of high-level graft. No more labyrinthine petitions.

Motives and Machinations: Who’s Really Protecting Whom?

Remulla’s move is part genuine reformer, part institutional power play, and part political theater. Good. Even if ambition and legacy are mixed in, the public interest is served the moment the AMLC is forced to choose between its banking “friends” and its mandate. The AMLC’s motivations are simpler: self-preservation, future BSP sinecures, and the bureaucratic religion of “never make a mistake that can be litigated.” They are gatekeepers who have become doormen for the gatecrashers.

The implicated personalities and their bankers? Their strategy is transparent: run out the six-month clock, file lift motions, exploit every procedural comma, and pray the next flood season distracts the public.

Endgame Scenarios: Happy Ending or the Usual Philippine Farce?

- Happy Ending (statistically impossible): Remulla’s pressure purges the captured elements. A joint task force forms. Forfeiture cases multiply. Bank secrecy is surgically reformed. Public trust is restored. And then I woke up.

- Philippine Reality (most probable): The conflict drags into endless hearings. Politically connected respondents deploy their influence. Some assets slip away. A few small-fry contractors are sacrificed. The structural contradiction remains untouched. Next year’s flood will wash away both the evidence and another layer of public cynicism.

- Cynical Compromise (the safe bet): A quiet backroom deal is struck. Cooperation is “promised.” David gets his BSP desk. Rhetoric cools. A few sacrificial lambs are offered to the media. The core rot—revolving door, six-month cap, regulatory capture—remains surgically untouched. The system, designed to fail upward, does exactly that.

We have seen this movie too many times. Remulla just turned on the lights in the theater. The question now is whether the rest of the audience will finally demand a different ending—or keep munching popcorn while the floodwaters rise again.

The ball is in the AMLC’s court. And this time, the public is watching the scoreboard.

Key Citations

A. Legal & Official Sources

- Philippines. 1987 Constitution of the Republic of the Philippines. 1987. Official Gazette of the Republic of the Philippines.

- Philippines. Congress. Republic Act No. 1405: An Act Prohibiting Disclosure of or Inquiry into, Deposits with any Banking Institution and Providing Penalty Therefor. 9 Sept. 1955. Lawphil.

- —. Republic Act No. 3019: Anti-Graft and Corrupt Practices Act. 17 Aug. 1960. Lawphil.

- —. Republic Act No. 6426: An Act Instituting a Foreign Currency Deposit System in the Philippines, and for Other Purposes. 4 Apr. 1974. Lawphil.

- —. Republic Act No. 6713: An Act Establishing a Code of Conduct and Ethical Standards for Public Officials and Employees. 20 Feb. 1989. Lawphil.

- —. Republic Act No. 6770: An Act Providing for the Functional and Structural Organization of the Office of the Ombudsman, and for Other Purposes. 17 Nov. 1989. Lawphil.

- —. Republic Act No. 7080: An Act Defining and Penalizing the Crime of Plunder. 12 July 1991. Lawphil.

- —. Republic Act No. 9160: An Act Defining the Crime of Money Laundering, Providing Penalties Therefor and for Other Purposes. 29 Sept. 2001. Lawphil.

- Republic Act No. 11521: An Act Further Strengthening the Anti-Money Laundering Law, Amending for the Purpose Republic Act No. 9160, Otherwise Known as the “Anti-Money Laundering Act of 2001”, as Amended. 29 Jan. 2021. Lawphil.

- Republic v. Eugenio Jr. G.R. No. 174629, 14 Feb. 2008. Lawphil.

- Subido Pagente Certeza Mendoza and Binay Law Offices v. Court of Appeals. G.R. No. 216914, 6 Dec. 2016. Lawphil.

B. News Reports

- Mendoza, John Eric. “Ombudsman Remulla Cites ‘Problem’ with AMLC Amid Flood Mess Probe.” Inquirer.net, 27 Mar. 2026.

- “Freeze Melts: CA Denies AMLC Bid, Opens Access to 100 Accounts Tied to Flood Control Scam.” Politiko, 25 Mar. 2026.

- “Forthwith” to Farce: How the Senate is Killing Impeachment—And Why Enrile’s Right (Even If You Can’t Trust Him)

- “HINDI AKO NAG-RESIGN!”

- “I’m calling you from my new Globe SIM. Send load!”

- “Mahiya Naman Kayo!” Marcos’ Anti-Corruption Vow Faces a Flood of Doubt

- “Meow, I’m calling you from my new Globe SIM!”

- “No Special Jail for Crooks!” Boying Remulla Slams VIP Perks for Flood Scammers

- “PLUNDER IS OVERRATED”? TRY AGAIN — IT’S A CALCULATED KILL SHOT

- “Several Lifetimes,” Said Fajardo — Translation: “I’m Not Spending Even One More Day on This Circus”

- “Shimenet”: The Term That Broke the Internet and the Budget

- “We Did Not Yield”: Marcos’s Stand and the Soul of Filipino Sovereignty

- “We Gather Light to Scatter”: A Tribute to Edgardo Bautista Espiritu

- $150M for Kaufman to Spin a Sinking Narrative

Leave a comment